How Much Will Your Disability Insurance Pay?

Most ER docs assume they're covered if they can't work. But knowing how much your disability insurance will actually pay — and where the gaps are — is what determines whether you can maintain your lifestyle if you're sidelined.

Here's how to do the math.

The 60% Rule

Most disability insurers cap total coverage at 60% of your gross income. That cap applies to the combined total of your group policy (through your employer) and any individual policy you hold on your own.

A Typical Situation

Most ER docs have group disability coverage through their employer. A common group policy covers 60% of gross income, up to $15,000/month — which works out to a maximum of $180,000/year.

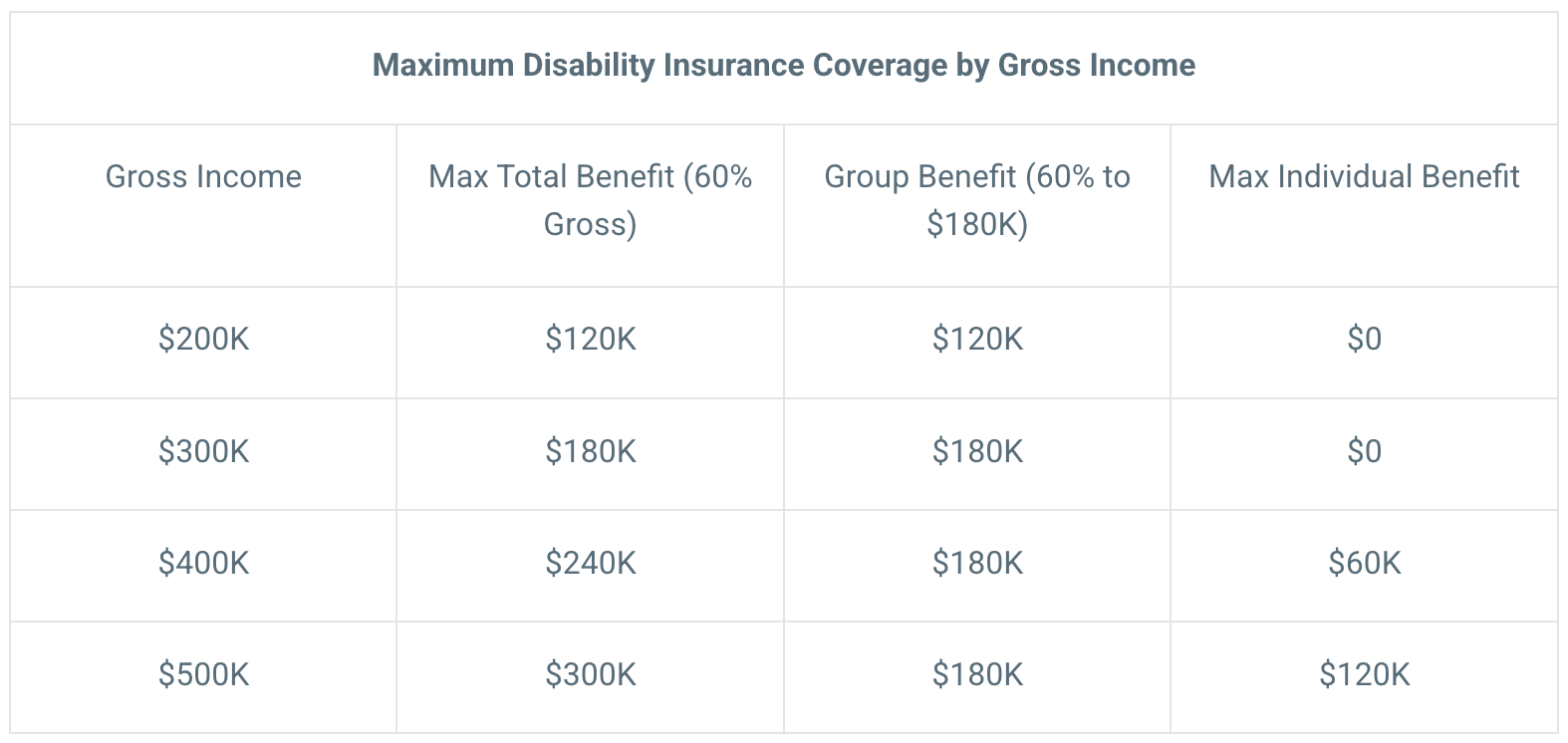

Payout Depends on Your Gross Income

How much you collect depends on what you were earning before you became disabled.

Using that same $180K/year ceiling:

Gross income below $300K/year? Your benefit is 60% of your gross — less than $180K/year.

Gross income of $300K/year? You hit the max: $300K × 60% = $180K/year.

Gross income above $300K/year? The group policy still caps out at $180K/year — you don't collect more just because you earn more.

Adding Individual Coverage

If you earn more than $300K/year and $180K/year wouldn't be enough to cover your expenses, you can apply for an individual disability policy to fill the gap.

The table below shows how group and individual coverage combine at different income levels:

The Bottom Line

If you're earning more than $300K/year — which describes most attending ER physicians — your group disability policy alone likely leaves a significant coverage gap. An individual policy can close that gap, but you need to know the numbers before you can make an informed decision.

Ready to put this into practice? If you're an ER physician or high-income professional looking for straightforward, evidence-based financial guidance, we'd love to connect. Schedule a free intro call with Yahara Wealth Management — no pressure, no sales pitch, just a conversation.

This article is for educational purposes only and does not constitute personalized financial, legal, or insurance advice. Individual disability policy terms, benefit caps, and eligibility requirements vary. Please consult a qualified financial advisor or insurance professional to evaluate your specific situation.