Locum Tenens Retirement Accounts: The Complete Guide

When you work locum tenens, retirement accounts are more complex, but there's more opportunity too.

Not to worry: We've done the research for you and compiled it here.

This guide gives you the confidence to enjoy the independence of locum tenens work.

As a result, you'll direct your career from a position of strength. You'll ask first: "What role can locums play for me?" Not: "How do locum tenens retirement accounts work?"

Then, when you want to work locums, go do it!

Introduction

You’re On Your Own

If you’re a W-2 employee, you likely have a retirement account (or two) available at your job. You can put in your own money, and your employer often puts something in too.

In locum tenens, you're NOT an employee of the hospital, the locums agency, or anyone else. Instead, you're a self-employed independent contractor.

This means you’re on your own. You must set up your own self-employed retirement account.

This also means you have more control and you can often put away more money!

Bottom Line

If you want to skip the details, here’s the bottom line.

You can use a solo 401(k) or a SEP IRA. (A SIMPLE IRA is not a good fit.)

Do the solo 401(k) unless you have a very good reason not to. The solo 401(k) has far more upside than the SEP. The downside is limited and manageable.

You can do it yourself or hire a pro to help you.

In our work with individual clients, we almost always use a solo 401(k) for locums docs.

Key Assumptions

This guide makes two key assumptions: You get a 1099 at tax time, and you’re taxed as a sole proprietor.

You Get A 1099 At Tax Time

If you get a 1099 at tax time:

You’re a self-employed independent contractor for tax purposes.

You can use a locum tenens retirement account to shelter some of your 1099 income from tax.

Sometimes docs say they’re doing locums because they’re working a few shifts a month somewhere, but they get a W-2 at tax time, not a 1099. “Per diem” usually means W-2 in our experience (but check for yourself).

If you get a W-2 at tax time:

You’re an employee for tax purposes.

You can’t use a locum tenens retirement account.

To avoid confusion, the rest of this guide refers to “1099 income,” not “locums income.”

You’re Taxed As A Sole Proprietor

When you have 1099 income, you’re taxed as a sole proprietor by default. And that’s good! Being taxed as a sole proprietor is almost always best.

As a sole proprietor, you file a Schedule C with your tax return. Schedule C calculates your net 1099 income. Revenue - expenses = net income.

The other option is to be taxed as an S corporation. You have to make a special election to be taxed this way. Some aspects of locum tenens retirement accounts work differently if you’re taxed as an S corp. We don’t cover that in this guide.

Solo 401(k)

This section covers the solo 401(k) in detail. The next section does the same for the SEP IRA.

A solo 401(k) is also called an individual 401(k), or i401(k) for short.

General

Many docs have a 401(k) at their W-2 job, or have had one in the past.

A solo 401(k) is simply a 401(k) plan that you set up for yourself. Your plan has only one participant, which is the owner, which is you!

A 401(k) is a qualified retirement plan under the tax code; a SEP IRA is not.

Qualified plans have more compliance requirements. In exchange, qualified plans are more flexible and powerful.

Reasons to Prefer a Solo 401(k)

There are several reasons to prefer a solo 401(k) over a SEP IRA. Here’s a list.

Higher Maximum Contribution

IRS rules set the maximum contribution you can make. Your max with a solo 401(k) is often higher than with a SEP, and never lower.

Lets You Do Backdoor Roth

You can make a backdoor Roth IRA contribution tax-free if your income is too high to contribute to Roth the regular way. But this strategy only works if you have no money in Traditional, SEP, or SIMPLE IRAs. If you do a SEP IRA for 1099 income, you can’t do a backdoor Roth IRA contribution tax-free anymore.

Lets You Do Mega Backdoor Roth

Strong savers with excellent cash flow can make very large Roth contributions using the Mega Backdoor Roth technique. Mega Backdoor Roth requires a 401(k) plan with very specific features. A SEP IRA won’t work.

More Flexible

A solo 401(k) is more flexible than a SEP IRA. For example:

It often takes less 1099 income to max a solo 401(k) than a SEP IRA.

A solo 401(k) can allow loans, but a SEP IRA can’t.

In the past, a solo 401(k) could allow Roth contributions, but a SEP IRA could not. Now, a SEP IRA can allow Roth contributions, but most SEP IRA providers don’t actually permit Roth yet.

Maximum Solo 401(k) Contribution: Initial Comments

Determining your maximum solo 401(k) contribution can be complex. This section offers some initial comments, to give you a sense up front.

Limit #1: Net 1099 Income

You can only contribute up to the amount of net 1099 income you made.

If you made $50K in net 1099 income, you can’t put more than $50K into a solo 401(k).

Other factors may limit you to less than that. But your net 1099 income caps you at $50K.

Limit #2: IRS Annual Additions

You can only contribute up to a limit specified by the IRS.

This is sometimes called the “annual additions limit,” or the “415 limit” after Section 415 of the Internal Revenue Code.

For 2024, the annual additions limit is $69K. This number increases with inflation over time.

Other factors may limit you to less than that. But the IRS caps you at $69K.

Two Types of Contributions

A 401(k) plan has two types of contributions: an employee contribution and an employer contribution.

As a locums doc, you’re the employee AND the employer, so it all comes out of your pocket.

So why should you care about employee contribution vs. employer contribution in a solo 401(k)?

Answer: Because the employee contribution and employer contribution each have rules for how much you can put in. Knowing the rules helps you determine your maximum solo 401(k) contribution.

Employee Contribution

Note: An employee contribution is sometimes called an “employee deferral,” and contributing is sometimes called “deferring.”

Maximum

The max employee contribution is $23,000 (2024).

If you’re age 50+, you can make an additional $7,500 “catch-up” employee contribution (2024), for a total max employee contribution of $30,500.

Earlier, we said the 2024 annual additions limit is $69,000. The $7,500 catch-up employee contribution does not count toward the annual additions limit.

So, if you’re age 50+ and you’re making the catch-up employee contribution, you can put up to $76,500 into your solo 401(k). $69,000 annual additions limit + $7,500 catch-up employee contribution = $76,500.

Pre-Tax or Roth

You can make your employee contribution pre-tax or Roth.

“Pre-tax” means you deduct your contribution on your taxes now, but you pay tax on money you take out in retirement. Save now, pay later.

“Roth” means you don’t deduct your contribution on your taxes now, but money you take out in retirement is tax-free. Pay now, save later.

Starting in 2026, the catch-up portion over age 50 must be Roth if you earn over $145,000.

You can make a Roth 401(k) employee contribution no matter what your income is.

Don’t confuse this with a Roth IRA, where you can’t contribute if your income is above a certain limit. Unless you do a backdoor Roth IRA, that is.

Limited By Employee Contributions Elsewhere

You get ONE employee contribution limit of $23,000 / $30,500 (2024) across all of the following workplace retirement accounts you may have:

401(k)

403(b)

Federal Thrift Savings Plan (TSP)

SIMPLE IRA

For example, if you’re under age 50 and you only have your solo 401(k), you can make a $23,000 employee contribution.

Now say you also have a 401(k) at a W-2 job, and you’re making a $23,000 employee contribution there to capture matching funds from the employer.

In this case, you can’t make an employee contribution to your solo 401(k). The same is true if you’re contributing $23,000 to a 403(b) or the federal TSP.

Not Limited By 457 Or IRA Contributions

A 457 plan is another type of workplace retirement plan. You can contribute to a 457 AND still make an employee contribution of $23,000 / $30,500 to a 401(k), 403(b), or the federal TSP.

Traditional and Roth IRAs are not workplace retirement plans. You can contribute to a Traditional or Roth IRA AND still make an employee contribution of $23,000 / $30,500 to a 401(k), 403(b), or the federal TSP.

Employer Contribution

Note: An employer contribution is sometimes called “profit sharing.”

Maximum

For quick math, the max employer contribution is roughly 20% of your net 1099 income. Net income is on line 31 of Schedule C of your tax return.

The exact max employer contribution is (Net Income - ½ Self-Employment Tax) * 20%. Half of the self-employment tax is on line 13 of Schedule SE of your tax return.

Pre-Tax or Roth

In the past, the employer contribution could only be pre-tax. As of 2023, the employer contribution can be Roth. Some solo 401(k) providers don’t permit Roth employer contributions yet though.

Not Limited By Contributions Elsewhere

The max employer contribution to your solo 401(k) is NOT limited by contributions to retirement plans of unrelated employers.

This means it doesn’t matter if you have a 401(k), 403(b), or federal TSP at a W-2 job. The max employer contribution to your solo 401(k) stays the same.

How To Determine Your Maximum Solo 401(k) Contribution

To find your maximum solo 401(k) contribution:

Figure your max employee contribution.

Figure your max employer contribution.

Add them together, and don’t exceed your net 1099 income or the IRS limit.

Below are two examples, first with $50K net 1099 income, then with $400K.

To keep it simple, we assume you’re under age 50 and you don’t have a W-2 job with a 401(k) or other retirement account.

Example 1: $50K Net 1099 Income

Maximum Employee Contribution

Because you’re under age 50 and you’re not making an employee contribution at a W-2 job, you can make a $23,000 employee contribution to your solo 401(k).

Maximum Employer Contribution

Your maximum employer contribution is (Net Income - ½ Self-Employment Tax) * 20%.

At $50K net 1099 income with no W-2 job, your tax return should show $7,065 of self-employment tax. Half of $7,065 is $3,533 (rounded).

($50,000 - $3,533) * 20% = $9,293 maximum employer contribution.

Note: you use your entire $50K net income to calculate your employer contribution. You don’t subtract your $23K employee contribution first.

Maximum Total Contribution

$23,000 max employee contribution + $9,293 max employer contribution = $32,293 total.

Now, make sure you can actually contribute this much.

Less than your net 1099 income of $50,000? Yes.Less than the IRS limit of $69,000? Yes.

So, your maximum total solo 401(k) contribution is $32,293.

Example 2: $400K Net 1099 Income

Maximum Employee Contribution

Because you’re under age 50 and you’re not making an employee contribution at a W-2 job, you can make a $23,000 employee contribution to your solo 401(k).

Maximum Employer Contribution

Your maximum employer contribution is (Net Income - ½ Self-Employment Tax) * 20%.

At $400K net 1099 income with no W-2 job, your tax return should show $31,619 of self-employment tax (2024). Half of $31,619 is $15,810 (rounded).

($400,000 - $15,810) * 20% = $76,838 maximum employer contribution.

Note: you use your entire $400K net income to calculate your employer contribution. You don’t have to subtract your $23K employee contribution first.

Maximum Total Contribution

$23,000 max employee contribution + $76,838 max employer contribution = $99,838 total.

Now, make sure you can actually contribute this much.

Less than your net 1099 income of $400,000? Yes.

Less than the IRS limit of $69,000? No. $99,838 is above the IRS limit.

So, your maximum total solo 401(k) contribution is $69,000.

Two Ways to Set Up Your Solo 401(k)

You set up a solo 401(k) plan in one of two ways:

Use a standard plan from a brokerage firm at no cost.

Get a custom plan from a provider for a fee.

Most locums docs should use a standard solo 401(k) plan.

You only need a custom plan if you want to do Mega Backdoor Roth or buy alternative investments. That isn’t most people.

The next two sections of this guide give you more detail on standard and custom plans.

Standard Solo 401(k) Plan

“Standard solo 401(k) plan” means a streamlined plan offered by a brokerage firm at no cost. Well-known options are Charles Schwab, Fidelity, and E-Trade. Vanguard exited the solo 401(k) space in 2024.

The brokerage firm provides the plan document and other paperwork. Setup is simple; just fill in a few blanks. You can invest in stocks, bonds, mutual funds, and exchange-traded funds (ETFs).

Standard solo 401(k) plans are less flexible in terms of plan features and investment options. Two key items of note:

You can’t do Mega Backdoor Roth.

You can’t buy alternative investments.

When you choose a brokerage firm, make sure their standard solo 401(k) plan meets your needs. For example, as of this writing:

Only E-Trade lets you take out a loan. This isn’t a big deal unless you have a specific reason to want a loan.

Only Fidelity doesn’t let you make Roth employee contributions. So, don’t use Fidelity unless you already invest there and really want to use Fidelity for everything.

No company mentioned above lets you make Roth employer contributions yet.

Custom Solo 401(k) Plan

If you want to do Mega Backdoor Roth or buy alternative investments, you need a plan from a custom solo 401(k) provider.

A custom solo 401(k) provider creates your plan document and provides ongoing compliance support. They don’t give you investment advice, nor do they act as a custodian of your investments.

Providers

There are many custom solo 401(k) providers. Two reputable ones that are a good fit for locums docs are My Solo 401(k) Financial and Nabers Group (no financial relationship with either). These firms support Mega Backdoor Roth and provide competent service at a reasonable rate.

Compliance Support

A solo 401(k) plan needs upkeep to stay in compliance. When choosing a custom provider, know what support they offer, and what’s included vs. what costs extra.

Below are the core services you need to stay compliant and save time and energy. My Solo 401(k) Financial and Nabers Group include all these services in their pricing.

Obtain federal employer ID number (EIN) for plan during setup

Include Mega Backdoor Roth feature

Include auto-enrollment feature to qualify for tax credit

Prepare Form 1099-R for distributions and conversions

Prepare Form 5500-EZ if plan > $250K in assets

Process loan requests

Support alternative investments

Update plan document when regulations change

Answer questions as needed

Investments

With a custom solo 401(k) plan, how you handle investments depends on what you’re buying.

Conventional Investments

Conventional investments are stocks, bonds, mutual funds, and ETFs. For these, you open an account at a brokerage firm, titled in the name of your solo 401(k).

Your custom solo 401(k) plan is governed by the plan document from your custom solo 401(k) provider. You’re not using the brokerage firm’s standard solo 401(k) plan document.

So, the brokerage firm only acts as custodian. This means they hold your investments and that’s it.

Charles Schwab, Fidelity, and E-Trade will all act as custodian when you use a custom solo 401(k) provider.Here is the proper account type at each custodian as of this writing.

Charles Schwab: Pension Trust

Alternative Investments

A full discussion of alternative investments in solo 401(k) plans is beyond the scope of this guide. Here’s our concise take.

Most Alternative Investments Don’t Make Sense

There’s no shortage of alternative investments out there. Precious metals, crypto, private equity, and the list goes on.

We don’t recommend most alternative investments, whether in your solo 401(k) or elsewhere.

Many are speculative.

Many require time and expertise you don’t have.

Most, if not all, are less transparent and liquid than conventional investments. Conventional investments are priced daily and can be traded easily and cheaply.

Most importantly, as a physician, you can reach financial independence by saving diligently and buying only conventional investments. So, there must be a very strong case for using an alternative investment.

Don’t Buy Real Estate In A Retirement Account

Real estate is the one alternative investment that can make sense in some cases.

In our view, you should only invest in real estate if:

You’ve built a solid base of conventional investments already.

You’re maxing out all retirement accounts available to you.

You have extra cash flow on top of that to invest in real estate.

You understand real estate and are comfortable with it.

If you do invest in real estate, don’t do it in a retirement account like your solo 401(k)!

Real estate is tax-sheltered on its own. Save your retirement accounts for conventional investments.

If You Insist

If you insist on buying alternative investments in your solo 401(k), here are a few comments.

First, rely heavily on your custom solo 401(k) provider to help you keep your plan in compliance. They won’t tell you what to invest in, but they should give guidance on items like titling investments in the name of your solo 401(k) and avoiding prohibited transactions. In the end, it’s on you to do everything right.

Second, a brokerage firm won’t hold alternative investments for you. You can take title in your capacity as trustee of your solo 401(k) plan, or have a custodian that specializes in alternative investments take title in the name of your solo 401(k) plan and act at your direction. Both ways have pros and cons. Ask your custom solo 401(k) provider for guidance.

Federal Employer ID Number (EIN)

You don’t need a federal employer ID number (EIN) for yourself, in order to set up a solo 401(k). You can use your Social Security number.

However, you do need an EIN for your solo 401(k) plan. This is because the plan is a separate entity from you for tax purposes.

If you use a standard solo 401(k) plan from a brokerage firm, you must obtain the EIN yourself on the IRS website. It’s free. If a financial advisor sets up your solo 401(k), they should obtain the EIN for you.

If you use a custom solo 401(k) provider, they may obtain the EIN for you. Choose a provider that does.

If you’re getting your own EIN, follow the IRS’s tips on how to get an EIN for your solo 401(k). Save the confirmation screen AND the confirmation letter. This is your only chance to get copies.

Deadlines

This section discusses three important solo 401(k) deadlines: tax return, plan setup, and contribution.

Tax Return Deadline

When it comes to solo 401(k)s, you see references to the tax return deadline “without extensions” and “with extensions.”

As we said earlier, this guide assumes you’re taxed as a sole proprietor. So, your tax return deadline without extensions is April 15th.

You can request an extension, which gives you until October 15th to file. So, your tax return deadline with extensions is October 15th. (You still have to pay any tax due by April 15th though!)

“With extensions” and “plus extensions” mean the same thing.

Solo 401(k) Setup Deadline

The solo 401(k) setup deadline for a given tax year is the tax return deadline plus extensions.

Example: For your 2024 tax return, the tax return deadline plus extensions is October 15th, 2025. So, you have until October 15th, 2025 to set up a solo 401(k) plan for tax year 2024.

You must actually file for an extension of your tax return, if you want to have until October 15th to set up your solo 401(k).

Solo 401(k) Contribution Deadline

The deadline to make solo 401(k) contributions is as follows.

For employee contributions:

In the first plan year:

If you signed the paperwork to establish your plan by December 31st, you have until the tax return deadline plus extensions (October 15th).

If you signed after December 31st, you have until the tax return deadline WITHOUT extensions (April 15th).

In future years, you have until the tax return deadline plus extensions (October 15th).

For employer contributions:

You always have until the tax return deadline plus extensions (October 15th).

You must actually file for an extension of your tax return, if you want to have until October 15th to make contributions.

Compliance Tasks

Certain tasks must be performed to keep your solo 401(k) in compliance over time. They aren’t hard, but you should be aware of them.

Keep Plan Document Up To Date

Your plan document must be kept up to date to reflect regulatory changes.

If you use a standard solo 401(k) plan, the brokerage firm will update its plan document. If you have a custom solo 401(k), your custom provider will update your document.

File Form 5500-EZ If Needed

If your solo 401(k) has over $250,000 in it on December 31st, you must file Form 5500-EZ by July 31st of the following year. This two-page form reports basic information about your plan, such as asset level and contributions made.

If you use a standard solo 401(k) plan, you must prepare Form 5500-EZ yourself. If a financial advisor manages your solo 401(k), they should prepare the form for you.

If you have a custom solo 401(k), your custom provider should prepare Form 5500-EZ for you. Choose a provider that does.

File Form 1099-R For Distributions

If you have a reportable distribution from your solo 401(k), you must file Form 1099-R by January 31st of the following year to tell the IRS about it.

If you use a standard solo 401(k) plan, the brokerage firm will issue Form 1099-R. If you use a custom plan, your custom provider should issue Form 1099-R. Choose a provider that does.

Say you’re working and putting money into your solo 401(k), not taking money out. You can still have a reportable distribution that requires Form 1099-R. Examples:

Converting pre-tax money to Roth within your solo 401(k) plan.

Converting voluntary after-tax contributions to Roth.

Making a Roth employer contribution.

Reporting Contributions on Your Tax Return

This section explains how to report solo 401(k) contributions on your tax return.

Pre-Tax Contributions

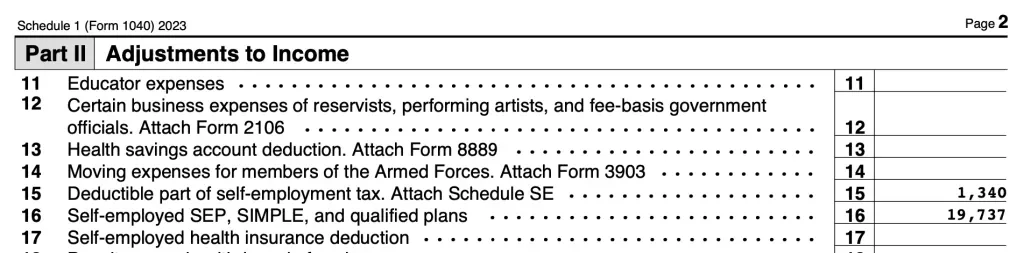

You deduct pre-tax contributions (employee and employer) on Form 1040, Schedule 1, Line 16. This is the line for “Self-employed SEP, SIMPLE, and qualified plans.”

This locums doc made $19,737 of pre-tax solo 401(k) contributions for tax year 2023.

Roth Contributions

Roth employee contributions don’t go on your tax return at all.

Roth employer contributions are handled as follows:

Deduct the Roth employer contribution on Form 1040, Schedule 1, Line 16 for the tax year for which you make the contribution.

Report the Roth employer contribution as taxable income on Form 1040, Lines 5a and 5b for the calendar year in which you make the contribution.

Clear as mud? Thought so. Here’s an example.

It’s April 1st, 2025 and your 2024 tax return is almost complete. You decide to make a $20,000 Roth employer contribution for tax year 2024.

Deduct $20,000 on your 2024 tax return. This is because you made the contribution for tax year 2024.

Report $20,000 of taxable income on your 2025 tax return. This is because you made the contribution in calendar year 2025.

Your solo 401(k) plan would issue a 2025 Form 1099-R by January 31st, 2026 to report the $20,000 of taxable income to the IRS.

Voluntary After-Tax Contributions (Mega Backdoor Roth)

Voluntary after-tax contributions (VATC) don’t go on your tax return at all.

You make VATC as Step 1 of Mega Backdoor Roth. Step 2 is to convert the VATC to Roth. You can make the conversion in one of two ways:

Convert within your solo 401(k).

Convert by rolling over the VATC from your solo 401(k) into a Roth IRA.

You report the conversion of VATC to Roth on your tax return, but it isn’t taxable. Specifically, you report the amount converted on Line 5a of Form 1040, but enter $0 on Line 5b (taxable amount), and write ROLLOVER next to Line 5b.

Your solo 401(k) plan would also issue a Form 1099-R to report the conversion to the IRS.

Tax Credit For Setting Up A Solo 401(k)

The government offers tax credits to motivate employers to set up 401(k) plans for their employees.

As a locums doc with no employees, there is one credit you may qualify for: the Small Employer Auto-Enrollment Credit.

Bottom Line

This tax credit is worth $1,500. You can only get it if you have a custom 401(k) plan.

If a standard solo 401(k) plan meets your needs, stick with that. It’s simpler. A $1,500 credit isn’t worth switching to a custom 401(k) plan.

If you want a custom 401(k) anyway, the $1,500 credit pays for the custom provider’s setup fee plus a few years of service!

If you already have a custom 401(k), you can amend your plan to add auto-enrollment now and get the credit.

Further Detail

The Small Employer Auto-Enrollment Credit is $500 for each of the first three years that a 401(k) plan has an auto-enrollment feature. $500 x 3 years = $1,500 total value of credit.

An auto-enrollment feature automatically enrolls new employees in a 401(k) plan unless they opt out. This gets a lot of people to save that otherwise wouldn’t. Powerful stuff!

As a locums doc, you have no employees besides yourself, but you can still include an auto-enrollment feature in your solo 401(k) plan and take the tax credit.

Standard solo 401(k) plans from Charles Schwab, Fidelity, and E-Trade don’t have an auto-enrollment feature as of this writing. Thus, you can’t take the credit if you have a standard solo 401(k) plan.

A custom 401(k) provider should include the auto-enrollment feature so you can take the credit.

The credit is available for new and existing plans. If you already have a custom 401(k) plan, have your provider amend the plan to add auto-enrollment, and you can claim the credit.

SEP IRA

This section covers the SEP IRA in detail.

General

A SEP IRA is an alternative to a 401(k) plan. SEP stands for Simplified Employee Pension.

Unlike a 401(k) plan, a SEP IRA is not a qualified retirement plan under the tax code.

This means the SEP has minimal compliance requirements. But it also means the SEP is less flexible and powerful.

Reasons to Prefer a SEP IRA

In our work with individual clients, we almost always use a solo 401(k) for locums docs.

With that said, this section covers reasons to prefer a SEP IRA over a solo 401(k). We’ll break this down into good reasons and bad ones.

Good Reasons to Prefer a SEP

It’s OK to choose a SEP IF you’ve compared the pros and cons of a solo 401(k) and a SEP IRA for your specific situation.

In our experience, most people haven’t done this.

Yes, the lower compliance burden of the SEP is nice. But the tradeoff is only worth it in this VERY limited case:

You’re satisfied with the maximum contribution a SEP offers you, even if it’s lower than your solo 401(k) max would be; AND

You think you’ll still feel this way in the future; AND

You don’t want to make backdoor Roth or Mega Backdoor Roth contributions; AND

You think you’ll still feel this way in the future; AND

You don’t want to handle solo 401(k) compliance tasks yourself; AND

You don’t have a professional to do solo 401(k) compliance tasks for you. This could be a custom solo 401(k) provider, or a good financial advisor if you use a standard solo 401(k) from a brokerage firm.

Note: You can go with a SEP now and switch to a solo 401(k) later. But it’s easier to choose once and be done with it.

Bad Reasons to Prefer a SEP

It’s bad if you default to a SEP IRA because:

You’ve heard of a SEP IRA but not a solo 401(k).

You don’t know how a solo 401(k) works.

You haven’t compared a solo 401(k) and a SEP IRA for your specific situation.

It’s even worse if your CPA or financial advisor defaults to a SEP IRA for the same reasons! They’re supposed to know better. But it happens. A lot, actually.

Maximum SEP IRA Contribution: Initial Comments

Your maximum SEP contribution starts off with the same two limits as the solo 401(k): net 1099 income and IRS annual additions.

You can only contribute up to the amount of net 1099 income you made. And you can only contribute up to the IRS annual additions limit, which is $69K for 2024.

With a SEP IRA, there is no additional “catch-up” contribution if you’re age 50+. The limit is $69K in 2024, regardless of age.

Only an Employer Contribution

With a SEP IRA, you can only make an employer contribution. There is no employee contribution.

This is why your SEP IRA maximum total contribution is sometimes less than with a solo 401(k).

The max employer contribution is the same for a SEP and a solo 401(k).

But the solo 401(k) also allows an employee contribution, while the SEP doesn’t.

Employer Contribution

The employer contribution works the same for a SEP IRA as it does for a solo 401(k). For clarity, we recap the main points below.

Maximum

For quick math, the max employer contribution is roughly 20% of your net 1099 income. Net income is on line 31 of Schedule C of your tax return.

The exact max employer contribution is (Net Income - ½ Self-Employment Tax) * 20%. Half of the self-employment tax is on line 13 of Schedule SE of your tax return.

Pre-Tax or Roth

In the past, the employer contribution could only be pre-tax. As of 2023, the employer contribution can be Roth. Standard SEP IRA plans from Charles Schwab, Fidelity, and E-Trade don’t allow Roth employer contributions as of this writing.

Not Limited By Contributions Elsewhere

The max employer contribution to your SEP IRA is NOT limited by contributions to retirement plans of unrelated employers.

This means it doesn’t matter if you have a 401(k), 403(b), or federal TSP at a W-2 job. The max employer contribution to your SEP IRA stays the same.

How To Determine Your Maximum SEP IRA Contribution

To find your maximum SEP IRA contribution:

Figure your max employer contribution.

Don’t exceed your net 1099 income or the IRS limit.

Below are two examples, first with $50K net 1099 income, then with $400K.

Example 1: $50K Net 1099 Income

Your maximum employer contribution is (Net Income - ½ Self-Employment Tax) * 20%.

At $50K net 1099 income with no W-2 job, your tax return should show $7,065 of self-employment tax. Half of $7,065 is $3,533 (rounded).

($50,000 - $3,533) * 20% = $9,293 maximum employer contribution.

Now, make sure you can actually contribute this much.

Less than your net 1099 income of $50,000? Yes.

Less than the IRS limit of $69,000? Yes.

So, your maximum SEP IRA contribution is $9,293.

Note: With a solo 401(k), your max would have been $32,293! $9,293 employee + $23,000 employee.

Example 2: $400K Net 1099 Income

Your maximum employer contribution is (Net Income - ½ Self-Employment Tax) * 20%.

At $400K net 1099 income with no W-2 job, your tax return should show $31,619 of self-employment tax (2024). Half of $31,619 is $15,810 (rounded).

($400,000 - $15,810) * 20% = $76,838 maximum employer contribution.

Now, make sure you can actually contribute this much.

Less than your net 1099 income of $400,000? Yes.

Less than the IRS limit of $69,000? No. $76,838 is above the IRS limit.

So, your maximum SEP IRA contribution is $69,000.

Note: With a solo 401(k), your max would also be $69,000. We would still recommend a solo 401(k) though!

Use A Standard SEP IRA

You set up a SEP IRA in one of two ways:

Use a standard SEP IRA from a brokerage firm at no cost.

Get a custom SEP IRA from a provider for a fee.

Use a standard SEP IRA from a brokerage firm.

You only need a custom SEP IRA if you want to buy alternative investments. As we discussed earlier, real estate is the only alternative investment that can make sense in certain cases. But you don’t want to buy real estate in a SEP IRA, for two reasons.

First, real estate is tax-sheltered on its own. Save your retirement accounts for conventional investments.

Second, if you insist on buying real estate in a retirement account, definitely use a solo 401(k), not a SEP IRA.

Most real estate investments are financed with debt. If you buy debt-financed real estate in an IRA, including a SEP IRA, the IRA has unrelated debt-financed income (UDFI) that is subject to unrelated business income tax (UBIT). But a solo 401(k) is not subject to this tax!

Standard SEP IRA

“Standard SEP IRA” means a streamlined SEP IRA offered by a brokerage firm at no cost. Well-known options are Charles Schwab, Fidelity, Vanguard, and E-Trade.

The brokerage firm provides the plan document and other paperwork. Setup is simple; just fill in a few blanks. You can invest in stocks, bonds, mutual funds, and exchange-traded funds (ETFs).

No Employer ID Number

You don’t need a federal employer ID number (EIN) for a SEP IRA.

Deadlines

This section discusses three important SEP IRA deadlines: tax return, plan setup, and contribution.

Tax Return Deadline

As discussed earlier, your tax return deadline without extensions is April 15th.

You can request an extension, which gives you until October 15th to file. So, your tax return deadline with extensions is October 15th. (You still have to pay any tax due by April 15th though!)

SEP IRA Setup Deadline

The SEP IRA setup deadline is the tax return deadline plus extensions.

You must actually file for an extension of your tax return, if you want to have until October 15th to set up your SEP IRA.

SEP IRA Contribution Deadline

The SEP IRA contribution deadline is also the tax return deadline plus extensions.

You must actually file for an extension of your tax return, if you want to have until October 15th to contribute to your SEP IRA.

Compliance Is Minimal

Compliance is minimal with a SEP IRA. The brokerage firm will file Form 1099-R for you with the IRS for reportable distributions. You don’t need to maintain a plan document or file Form 5500-EZ. Just don’t exceed your maximum contribution.

Reporting Contributions on Your Tax Return

You deduct pre-tax contributions (employee and employer) on Form 1040, Schedule 1, Line 16. This is the line for “Self-employed SEP, SIMPLE, and qualified plans.”

Standard SEP IRAs from brokerage firms don’t permit Roth contributions yet.

Voluntary after-tax contributions aren’t allowed in SEP IRAs. This means Mega Backdoor Roth is not possible with a SEP IRA.

No Tax Credit

You don’t get a tax credit for setting up a SEP IRA.

A Financial Advisor's Role With Your Locums Retirement Account

If you have a financial advisor, or are considering one, they should know locum tenens retirement accounts inside out. Many financial advisors do not.

A financial advisor should handle your locum tenens retirement account from start to finish. They should:

Compare a solo 401(k) and a SEP IRA for your individual situation.

Select the right account and set it up for you.

Calculate your maximum contribution each year and help you fund it.

Manage the investments in the account if you want them to.

Do NOT let a financial advisor, or an accountant, default to a SEP IRA without explaining why they recommend it over a solo 401(k).

Conclusion

We hope this guide has saved you time and energy. Now you can enjoy the independence of locums work without worrying about retirement accounts. When you want to work locums, go do it!

Ready to put this into practice? If you're an ER physician or high-income professional looking for straightforward, evidence-based financial guidance, we'd love to connect. Schedule a free intro call with Yahara Wealth Management — no pressure, no sales pitch, just a conversation.

This material is for educational and informational purposes only and should not be construed as personalized tax, legal, or investment advice. Tax laws are complex and subject to change; consult a qualified tax professional or financial advisor regarding your individual situation. Any hypothetical examples are for illustrative purposes only and do not represent actual client outcomes or guaranteed results.