Managing Federal Student Loans During Residency: What You Should Know

Managing Student Loans During Residency

Managing student loans during residency is one of the most overlooked financial decisions you'll make — and it has real, lasting consequences.

This article assumes the following:

You have federal loans.

You're early in residency. For now, the goal is to manage your existing loans wisely while you wait. Once you've locked in your first attending position, you'll have the full picture you need to make longer-term decisions about refinancing or pursuing forgiveness.

Your Two Options

As a resident, you have two basic choices for managing your federal student loans:

Forbearance. Many residents choose this because they feel they can't afford to make payments.

Repayment status. This is the route we recommend. Your payment can be very low — or even $0 — and you preserve far more options down the road.

Forbearance

Going into forbearance means requesting temporary relief from making payments. It won't hurt your credit — but interest keeps accruing the entire time, and you make zero progress on your loans.

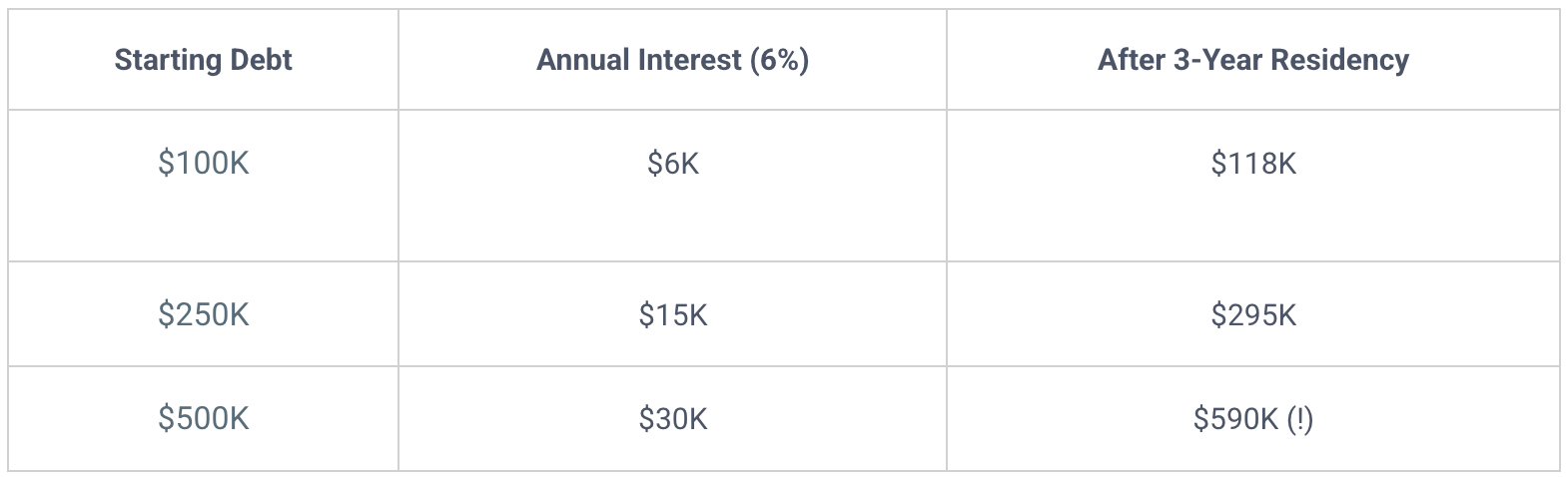

That interest adds up fast. Depending on your loan balance, here's what three years of forbearance at 6% looks like:

One important distinction: forbearance is not the same as default. Default means you've stopped making payments and haven't requested any relief. That's genuinely harmful to your credit. If you're already in default, you still have options — but act quickly.

Repayment Status

Entering repayment status simply means choosing a repayment plan. Depending on which plan you select, your monthly payment might be surprisingly low — even $0.

There are several repayment plans available.

Standard Plan

The Standard Plan sets a fixed payment over 10 years. For most residents with significant debt, this is simply unaffordable. With $250,000 in debt at 6%, the monthly payment would be roughly $2,776.

Plans with Lower Payments

Other plans make residency more manageable in one of two ways:

Extending repayment beyond 10 years, which lowers the monthly payment.

Basing your payment on your income — these are called income-driven repayment (IDR) plans.

For most residents, an income-driven plan is the right choice.

Our Recommendations

Rule #1: Enter repayment status — don't default to forbearance.

Any payment you make is progress. Under an income-driven plan, your payment as a resident could be very low or even $0. There's little reason to choose forbearance when a $0 IDR payment accomplishes the same thing — without the lost time toward forgiveness.

Rule #2: Before choosing forbearance, run the numbers.

Use the federal loan simulator to estimate your income-driven payment first. Only consider forbearance if both of the following are true:

Your income-driven payment is greater than $0.

You genuinely can't afford that payment — for example, because you're carrying high-interest credit card debt that needs to be paid down first.

If only one of those conditions applies, forbearance is not the right move.

Rule #3: Choose an income-driven plan.

There are two strong reasons to go this route:

Your payment should be affordable on a resident's salary, especially if you keep other living expenses in check.

Under current program rules, every month on an income-driven plan — even months whereSchedule a free intro call your payment is $0 — counts toward future loan forgiveness. You may not pursue forgiveness once you're an attending, but there's no reason to close that door now.

Ready to put this into practice? If you're an ER physician or high-income professional looking for straightforward, evidence-based financial guidance, we'd love to connect. Schedule a free intro call with Yahara Wealth Management — no pressure, no sales pitch, just a conversation.

This content is for educational purposes only and does not constitute personalized financial, tax, or legal advice. Federal student loan rules and repayment plan availability are subject to change. Consult a qualified financial advisor before making decisions about your student loans.