The Best Accounts To Leave To Charity (Not To Heirs)

The best accounts to leave to charity are pre-tax accounts — like a Traditional IRA or 401(k). Your heirs would owe income tax on every dollar they withdraw. A charity wouldn't pay a dime.

Heirs, Charities, and Uncle Sam

At the end of the day, your money can only go three places:

You can spend it.

You can give it to heirs and charities.

You can give it to the IRS by paying taxes.

The goal is simple: leave more to heirs and charities, and less to Uncle Sam. The way to do that is to leave your pre-tax accounts to charity — and your other accounts to your heirs.

Pre-Tax Accounts: The Basics

There are three types of investment accounts: pre-tax, tax-free, and taxable. Traditional IRAs and 401(k)s are the most common pre-tax accounts.

Withdrawals from pre-tax accounts are taxed as ordinary income — both during your lifetime and after your death:

Withdraw during your lifetime → you pay ordinary income tax.

Leave pre-tax accounts to your heirs → they pay ordinary income tax.

Withdrawals from Roth and taxable accounts are taxed more favorably, which matters a great deal when deciding who inherits what.

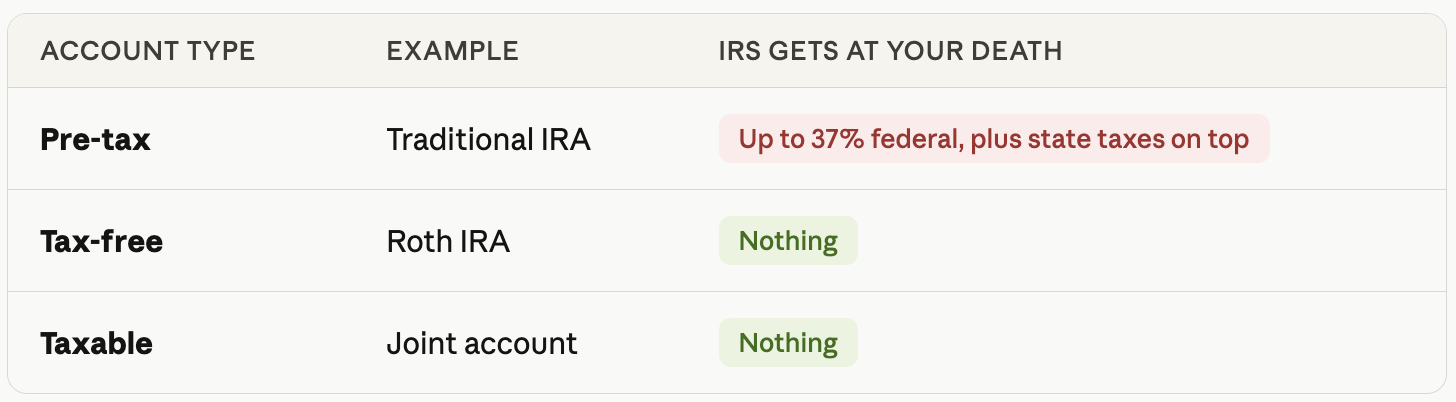

What Gets Taxed When Left To Heirs

Here's a snapshot of how much the IRS collects at your death depending on which account type you leave behind:

The IRS takes a large cut of pre-tax accounts because heirs pay ordinary income tax on every withdrawal.

This problem got worse with the SECURE Act. Non-spouse heirs generally must now withdraw the entire inherited balance within 10 years. They don't get to stretch distributions over a lifetime anymore — they have to take it all out within a decade, whether they need it or not.

If your kids are in their peak earning years, that inherited IRA gets stacked on top of their existing income. A $1 million pre-tax account could cost them roughly $400,000 in income taxes — assuming a 40% marginal rate (illustrative purposes only; actual tax liability will vary based on individual circumstances).

Leave Pre-Tax Accounts to Charity Instead

Charities pay no income tax. Leave that same $1 million pre-tax account to a charity, and the full $1 million goes to work for a cause you care about — nothing lost to taxes.

Then leave your other accounts to your heirs. Leave a $1 million Roth IRA to your kids, and they keep the entire $1 million.

The math is straightforward. Route the taxable accounts to tax-exempt recipients, and route the tax-free accounts to people who will benefit from that tax-free status.

Charitable Giving During Your Lifetime

This post focuses on the at-death strategy, but there are also ways to give charitably from pre-tax accounts while you're still alive:

Make Qualified Charitable Distributions (QCDs) from your IRA once you reach age 70½.

Earmark IRA funds for charity well before you die, in case you don't end up needing them for living expenses.

Both strategies can reduce your taxable income while supporting causes that matter to you.

Work With Yahara Wealth Management

Ready to put this into practice? If you're an ER physician or high-income professional looking for straightforward, evidence-based financial guidance, we'd love to connect. Schedule a free intro call with Yahara Wealth Management — no pressure, no sales pitch, just a conversation.

This article is for educational purposes only and does not constitute personalized tax, legal, or investment advice. Tax rules are complex and subject to change. Consult a qualified tax advisor or estate planning attorney regarding your specific situation. Yahara Wealth Management is a registered investment adviser in the State of Wisconsin.