The Best Accounts To Leave To Heirs (Not To Charity)

The best accounts to leave to heirs are tax-free accounts (like a Roth IRA) and taxable accounts — because your heirs pay no income tax on withdrawals from either.

Heirs and Charities vs. Uncle Sam

At the end of the day, your money can only go three places:

You can spend it.

You can give it to heirs and charities.

You can give it to the IRS by paying taxes.

The goal is simple: at your death, give more to the people you love and less to Uncle Sam. That means leaving tax-free and taxable accounts to human heirs, and leaving pre-tax accounts to charity.

Tax-Free and Taxable Accounts: The Basics

There are three types of investment accounts: pre-tax, tax-free, and taxable.

Withdrawals from tax-free accounts — like a Roth IRA or Roth 401(k) — are not subject to income tax. The same goes for taxable accounts, like an individual or joint brokerage account.

Pre-tax accounts are a different story. Withdrawals are taxed as ordinary income, which is far less favorable for your heirs.

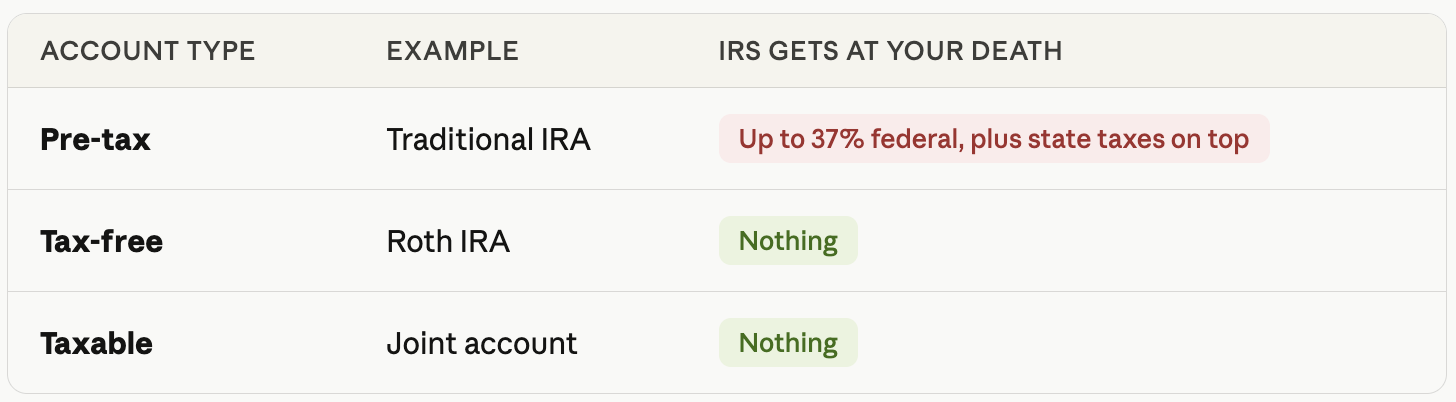

No Income Tax at Your Death

This table shows how much income tax the IRS collects at your death when you leave money to heirs:

The IRS gets nothing from your tax-free or taxable accounts at your death. Leave these to your heirs.

After Your Death

Tax-free and taxable accounts behave quite differently once inherited. Here's what to know.

Tax-Free Accounts

Roth IRAs and Roth 401(k)s are the best accounts to leave to heirs. Your heirs can let the money continue growing tax-free — and withdrawals, when they come, are also tax-free.

Spouse beneficiaries can treat the inherited Roth IRA as their own, letting it grow tax-free for the rest of their lives.

Non-spouse beneficiaries (your kids, for example) can let the money grow tax-free for up to 10 years. After that, they generally must withdraw the full balance. The withdrawal is still tax-free — but the tax-free compounding ends there.

It was even better before the SECURE Act, when non-spouse heirs could stretch withdrawals over their entire lifetimes. But 10 years of tax-free growth is still a significant advantage.

Taxable Accounts

Taxable accounts are also excellent assets to leave to heirs, thanks to the step-up in basis at death.

Here's how it works: when you die, the tax basis of your taxable accounts is "stepped up" to the fair market value on your date of death. That means your heirs can inherit the account and sell immediately with little or no capital gains tax — regardless of how much the investments appreciated during your lifetime.

Example: Your grandfather bought $10,000 of stock 50 years ago. At his death, that stock was worth $100,000. Because of the step-up in basis, your basis in the inherited stock becomes $100,000 — not $10,000. Sell it the next day, and your taxable gain is zero ($100,000 sale − $100,000 basis = $0).

Real estate and other tangible property also receives a step-up in basis at death.

Charitable Giving During Your Lifetime

If you want to give to charity while you're alive, taxable accounts offer a few powerful strategies:

Donate appreciated stock, deduct the full fair market value on your taxes, and pay zero capital gains tax.

Bunch your donations — give two years' worth every other year — if you typically take the standard deduction.

Ready to put this into practice? If you're an ER physician or high-income professional looking for straightforward, evidence-based financial guidance, we'd love to connect. Schedule a free intro call with Yahara Wealth Management — no pressure, no sales pitch, just a conversation.

This post is for educational purposes only and does not constitute personalized tax, legal, or investment advice. Tax rules are subject to change. Please consult a qualified tax or financial professional before making decisions based on this information. Yahara Wealth Management is a registered investment adviser in the state of Wisconsin.