The Three Types of Investment Accounts

Every investment account falls into one of three categories: pre-tax, tax-free, or taxable. The differences between them come down to one thing — taxes. Specifically, when you pay them, and on what. Understanding this distinction is foundational to building a tax-efficient portfolio.

Types of Investment Accounts

The three types are:

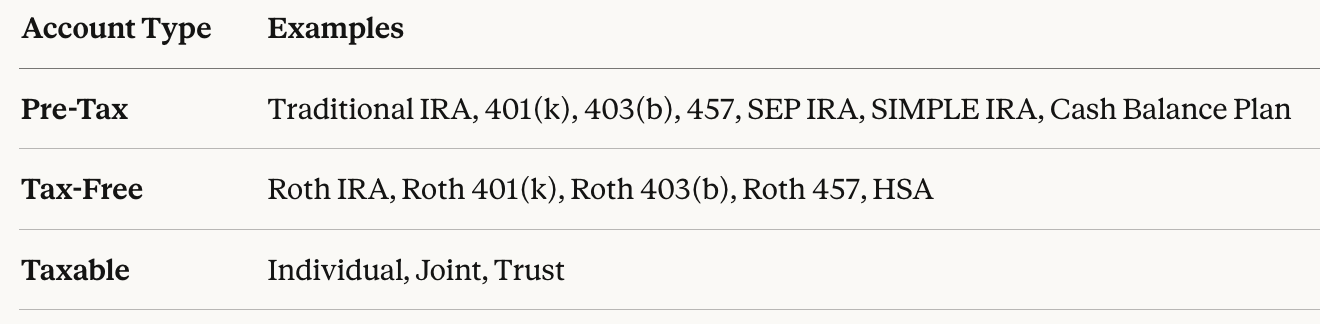

Pre-tax

Tax-free

Taxable

Pre-Tax and Tax-Free

Pre-tax and tax-free accounts are both commonly called "retirement accounts." The IRS gives them tax-favored status to encourage long-term wealth building.

These accounts can be opened through an employer or on your own. Both types carry contribution limits, which vary by account type and sometimes by income level. The limits also adjust upward with inflation over time.

Taxable

Taxable accounts are not retirement accounts and have no contribution limits. Anyone can open one — they're also commonly called brokerage accounts.

Examples

This table shows examples of each account type.

Tax Treatment

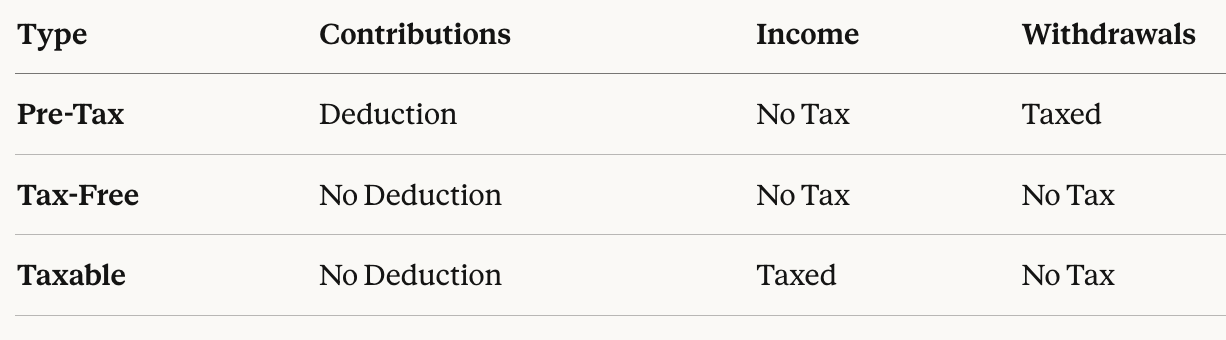

The tax treatment of each account type differs at three key points:

When money goes in (contributions)

While money is in (income)

When money comes out (withdrawals)

Contributions

Pre-tax accounts save you money on the front end — you get a tax deduction for every dollar you contribute. Contribute $20,000 to a pre-tax 401(k) at a 40% effective tax rate, and you'll save $8,000 on your tax return.

Tax-free and taxable accounts don't offer a deduction, so there's no upfront tax break. The benefit comes later.

The one exception is the Health Savings Account (HSA). An HSA is tax-free and gives you a deduction for contributions — making it one of the most tax-efficient accounts available.

Income

While money sits in an account, it can generate three types of income:

Dividends from stocks (or stock mutual funds)

Interest from bonds (or bond mutual funds)

Capital gains from selling investments at a profit

In pre-tax and tax-free accounts, none of this income affects your tax return. Dividends, interest, and capital gains all grow without being taxed year to year.

In taxable accounts, you owe tax on that income each year as it's generated.

Withdrawals

With pre-tax accounts, every dollar you withdraw is taxed as ordinary income — your original contributions and all the growth.

With tax-free accounts, qualified withdrawals are completely tax-free. No tax on contributions, no tax on growth. That's the tradeoff for not getting an upfront deduction — you pay tax on the seed, not the harvest. For more on when you can access these accounts, see:

With taxable accounts, withdrawals themselves don't trigger a tax bill. What triggers tax is the sale of an investment — if you sell at a gain, you owe capital gains tax. That tax is owed whether you leave the proceeds in the account or pull them out. The sale causes the tax, not the withdrawal.

Ready to put this into practice? If you're an ER physician or high-income professional looking for straightforward, evidence-based financial guidance, we'd love to connect. Schedule a free intro call with Yahara Wealth Management — no pressure, no sales pitch, just a conversation.

This article is for educational purposes only and does not constitute personalized investment, tax, or financial advice. Tax rules are complex and subject to change.